Learn how to create a budget that actually works, even if you’ve failed before. Discover why budgets fail, the 50/30/20 rule, zero-based budgeting, budgeting apps, common mistakes, and practical tips to finally take control of your finances.

How to Create a Budget That Actually Works (Even If You’ve Failed Before)

Managing your money doesn’t have to feel overwhelming. If you’ve ever created a budget only to abandon it a few weeks later, you’re far from alone.

Millions of people start budgeting with good intentions, only to find themselves slipping back into old spending habits.

The problem isn’t necessarily a lack of discipline—it’s often because the budgeting method simply doesn’t fit their lifestyle.

A budget shouldn’t make you feel restricted or guilty every time you spend money. Instead, it should give you confidence, clarity, and control over your finances.

The right budget allows you to pay your bills on time, save consistently, prepare for emergencies, and still enjoy life without constantly worrying about money.

The good news is that budgeting is a skill anyone can learn.

You don’t need to be a financial expert or earn a high income to make it work. What matters most is having a realistic plan that matches your goals and is easy enough to stick with month after month.

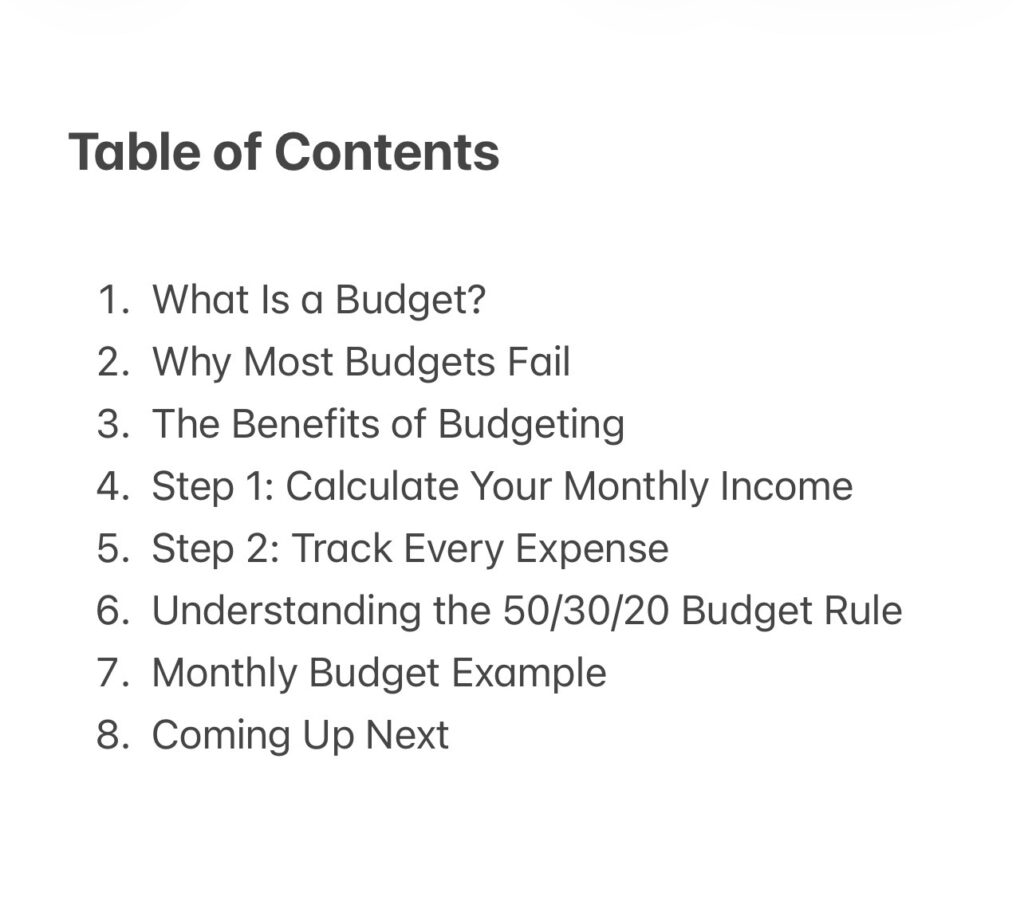

In this comprehensive guide, you’ll learn why most budgets fail, how to choose a budgeting method that suits your lifestyle, the popular 50/30/20 rule, zero-based budgeting, the best budgeting apps, common mistakes to avoid, and practical strategies to finally build a budget that works for you.

What Is a Budget?

A budget is simply a financial plan that tells your money where to go before you spend it.

Instead of wondering why your bank account is empty at the end of the month, budgeting helps you decide in advance how much money will be used for bills, groceries, transportation, savings, investments, and entertainment.

Think of your budget as a roadmap. Without one, you’re likely to spend based on emotions or impulse. With one, every dollar has a purpose.

Budgeting doesn’t mean saying “no” to everything you enjoy. It means saying “yes” to the things that matter most while avoiding unnecessary spending that doesn’t add value to your life.

Whether your goal is buying a home, paying off debt, traveling, or simply reducing financial stress, budgeting is the foundation that makes those goals achievable.

Why Most Budgets Fail

If you’ve tried budgeting before and failed, don’t be discouraged. The truth is that many traditional budgeting methods are unrealistic, making it difficult for people to stick with them.

Here are the biggest reasons budgets often fail.

1. They Are Too Restrictive

One of the most common mistakes is trying to eliminate all fun spending overnight.

For example, someone who normally spends $250 each month eating out may suddenly decide they’ll spend nothing at all.

While that sounds responsible, it’s rarely sustainable. After a few weeks, frustration builds, and many people end up overspending because they feel deprived.

A successful budget allows room for enjoyment while still helping you reach your financial goals.

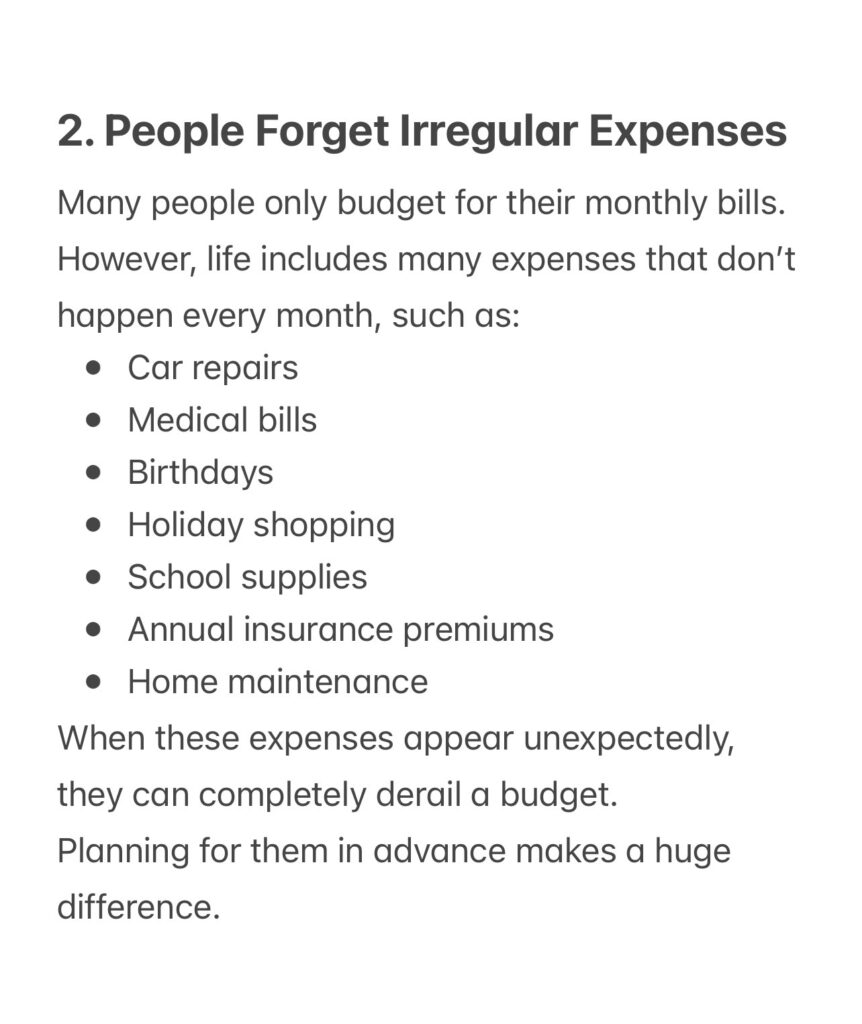

2. People Forget Irregular Expenses

Many people only budget for their monthly bills.

However, life includes many expenses that don’t happen every month, such as:

3. Not Tracking Spending

Creating a budget is only half the job.

You also need to monitor where your money actually goes.

Without tracking your expenses, it’s easy to underestimate how much you’re spending on things like food delivery, online shopping, or subscription services.

Even small purchases can add up significantly over a month.

4. Making the Budget Too Complicated

Some people create spreadsheets with dozens of spending categories, formulas, and charts.

While these may look impressive, they often become difficult to maintain.

The simpler your budgeting system is, the more likely you’ll continue using it.

Remember, consistency is more important than complexity.

5. Giving Up After One Bad Month

Many people abandon budgeting after a single month of overspending.

Unexpected expenses happen to everyone.

A budget isn’t meant to be perfect.

It’s a living financial plan that should be adjusted as your circumstances change.

Missing your budget one month doesn’t mean you’ve failed—it simply means it’s time to review and improve your plan.

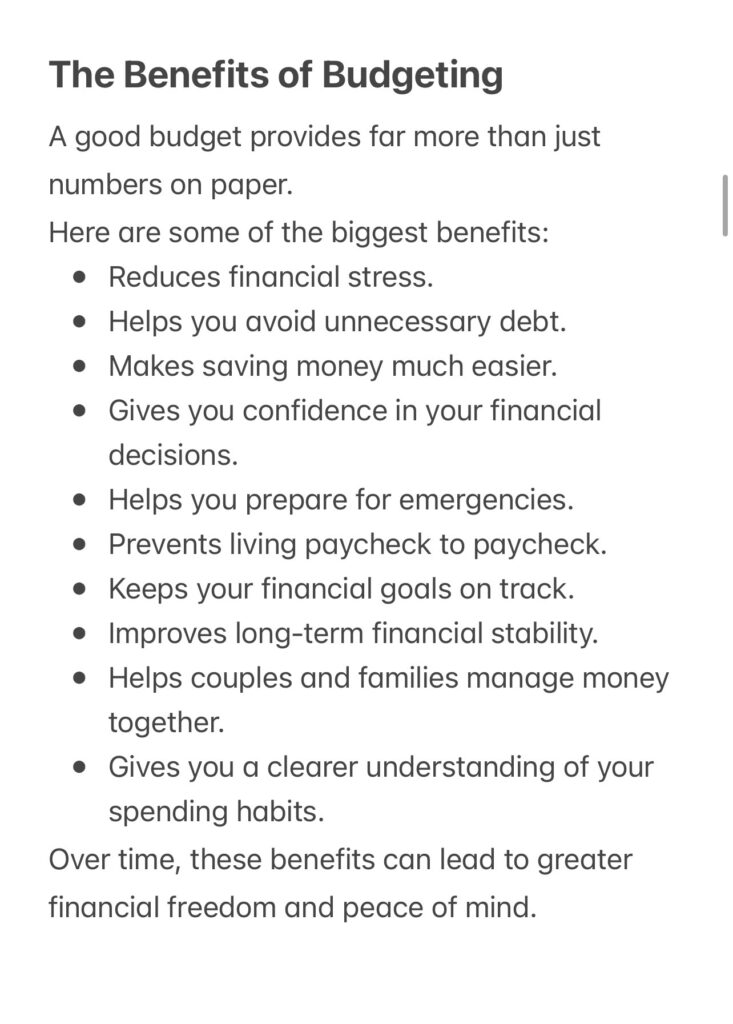

The Benefits of Budgeting

A good budget provides far more than just numbers on paper.

Here are some of the biggest benefits:

Step 1: Calculate Your Monthly Income

Before creating a budget, you need to know exactly how much money comes in each month.

Use your take-home income—the amount you receive after taxes and deductions.

Include income from:

If your income changes from month to month, calculate the average from your last six months to create a realistic estimate.

Having an accurate picture of your income helps you build a budget you can actually follow.

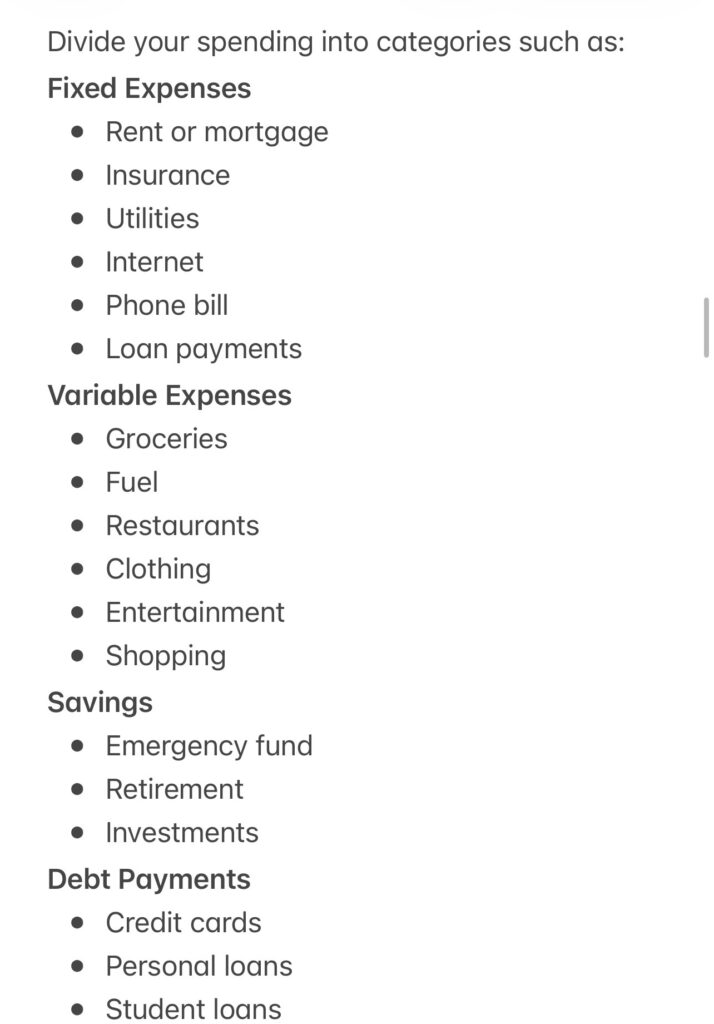

Step 2: Track Every Expense

The next step is understanding where your money currently goes.

Spend one month recording every expense, no matter how small.

Divide your spending into categories such as:

Fixed Expenses

Tracking your spending helps identify areas where you can cut back without sacrificing your quality of life.

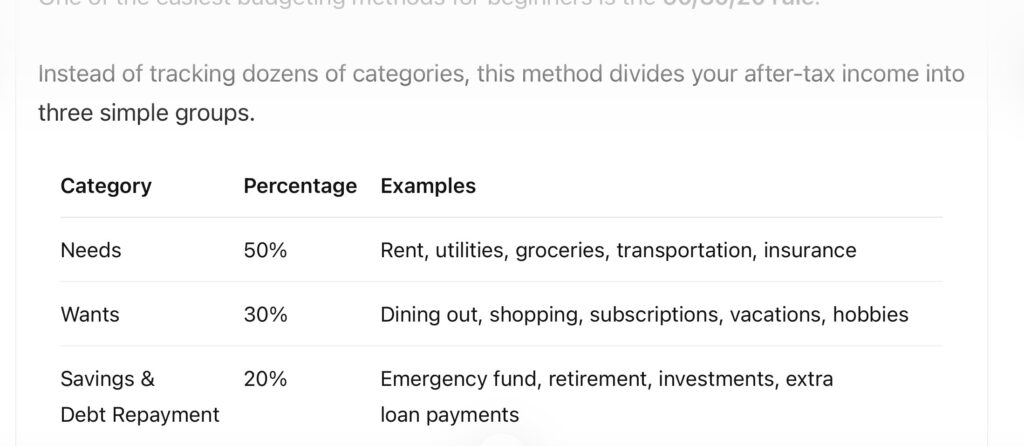

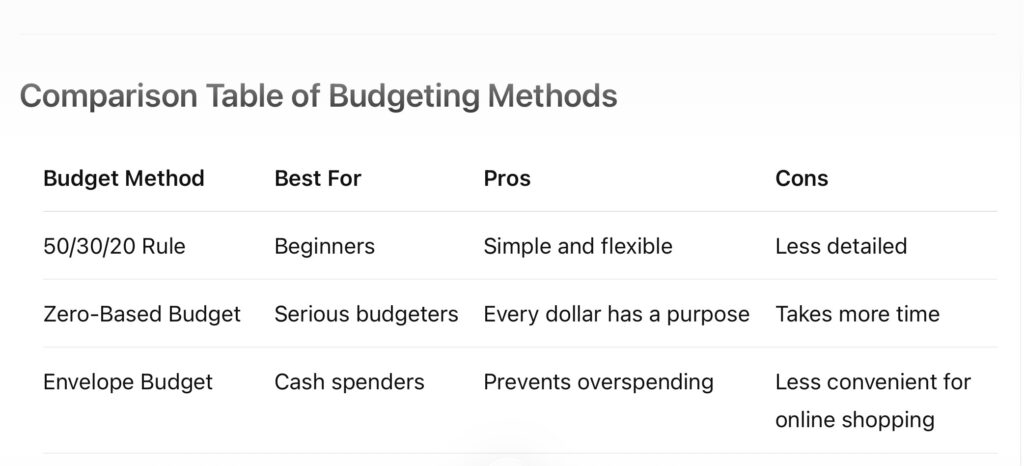

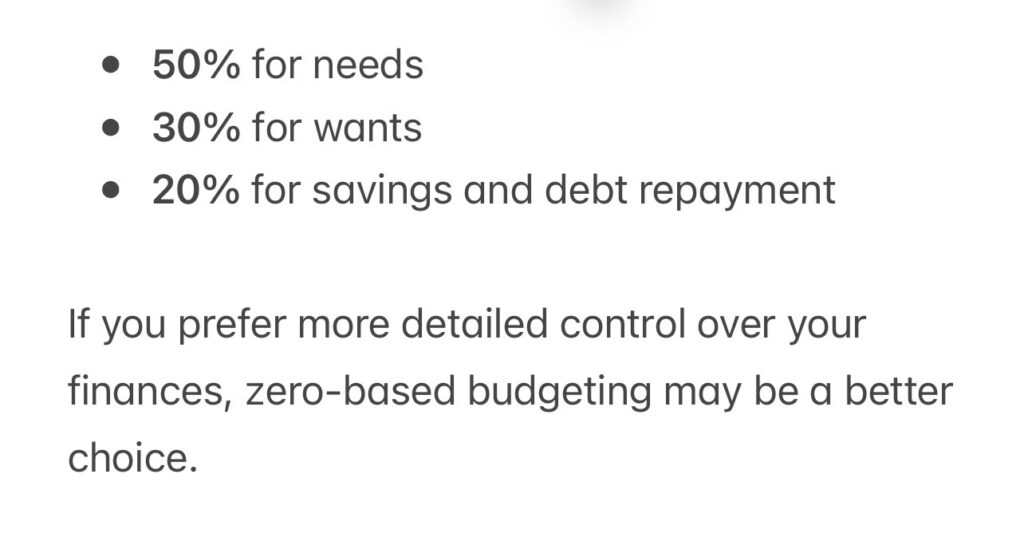

Understanding the 50/30/20 Budget Rule

One of the easiest budgeting methods for beginners is the 50/30/20 rule.

Instead of tracking dozens of categories, this method divides your after-tax income into three simple groups.

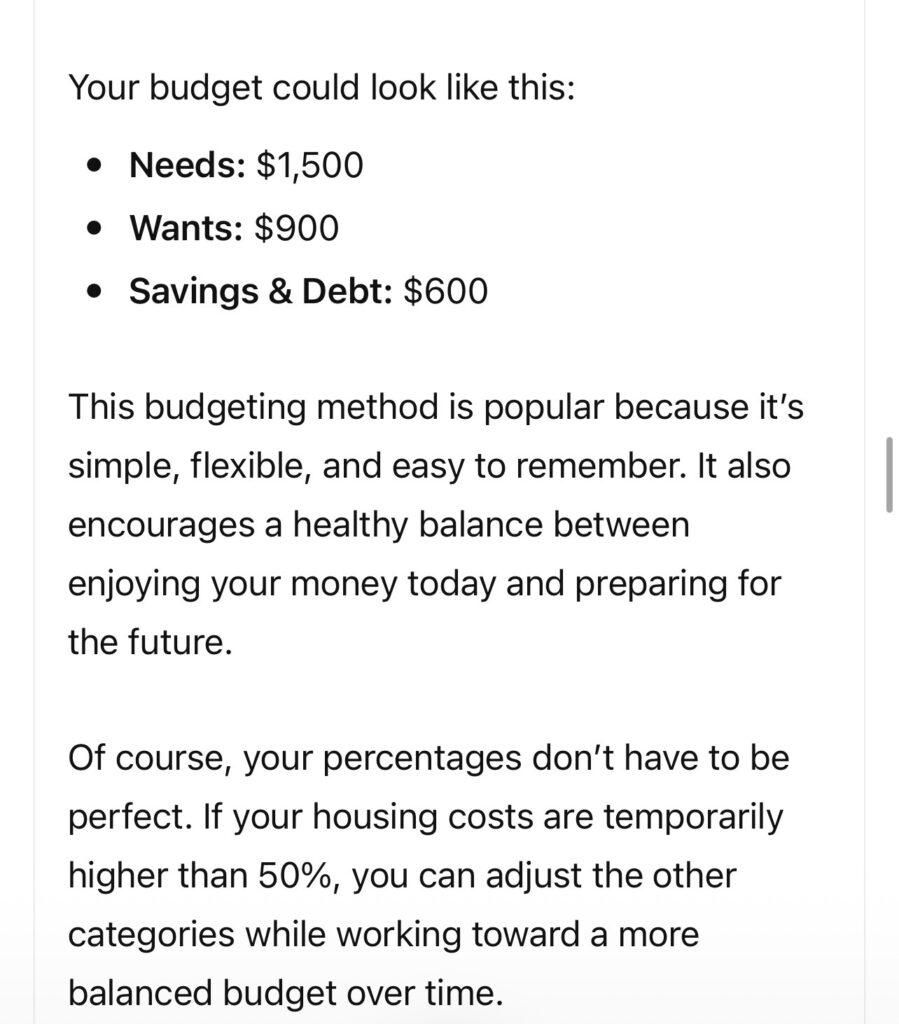

Example

Imagine your monthly take-home income is $3,000.

This budgeting method is popular because it’s simple, flexible, and easy to remember. It also encourages a healthy balance between enjoying your money today and preparing for the future.

Of course, your percentages don’t have to be perfect. If your housing costs are temporarily higher than 50%, you can adjust the other categories while working toward a more balanced budget over time.

Zero-Based Budgeting Explained

If you like having complete control over your finances, zero-based budgeting may be the perfect system for you.

Unlike the 50/30/20 rule, which focuses on percentages, zero-based budgeting gives every single dollar you earn a specific job.

At the beginning of each month, you assign all of your income to different categories until there is nothing left unassigned.

This doesn’t mean you should spend all your money.

Instead, every dollar is intentionally allocated—whether it’s for rent, groceries, savings, investing, debt repayment, or entertainment.

The goal is simple:

Income – Expenses – Savings = $0

Every dollar has a purpose.

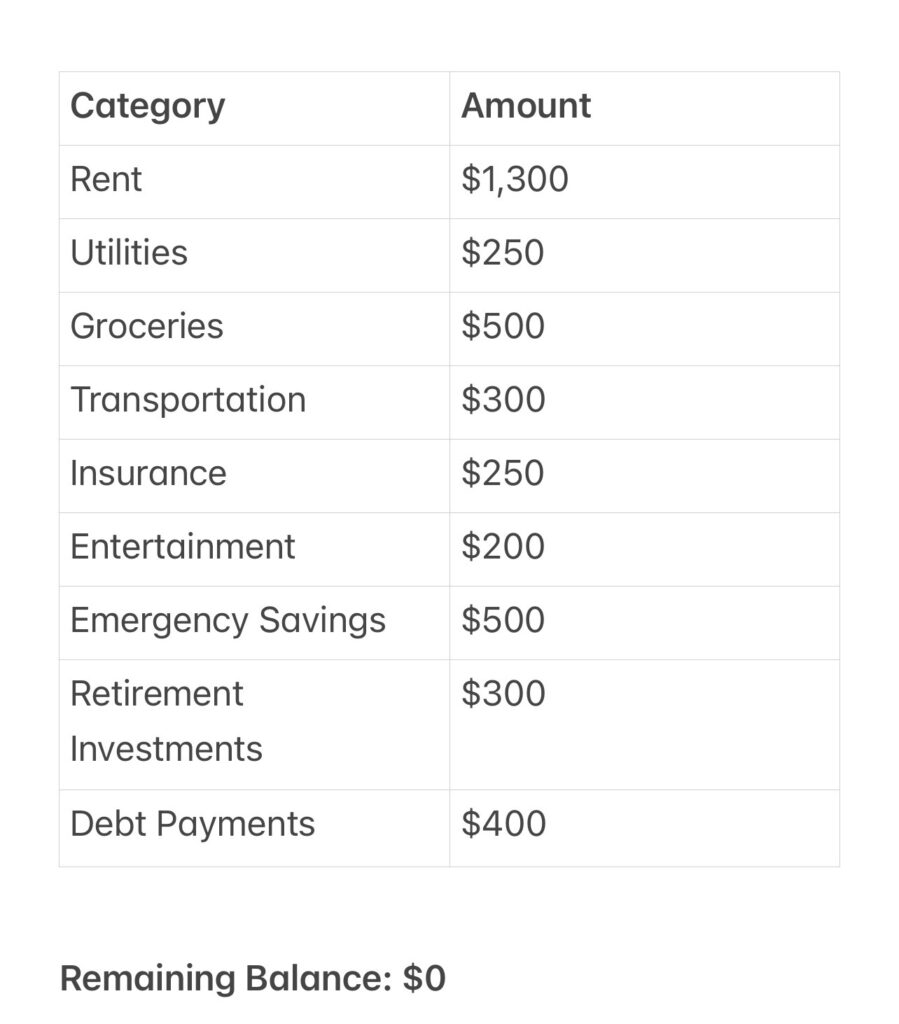

Zero-Based Budget Example

Imagine your monthly take-home income is $4,000.

Remaining Balance: $0

Nothing is left without a plan.

This budgeting method is excellent for people who want detailed control over their money and enjoy tracking their spending regularly.

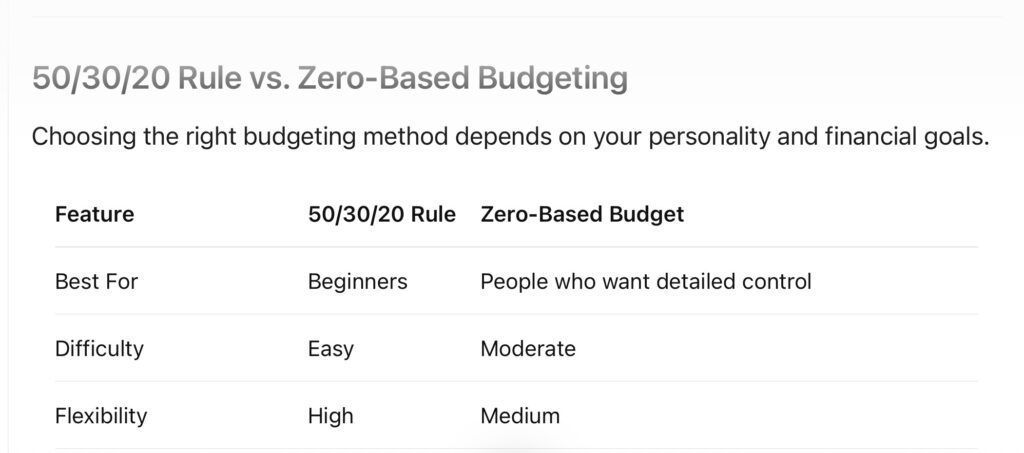

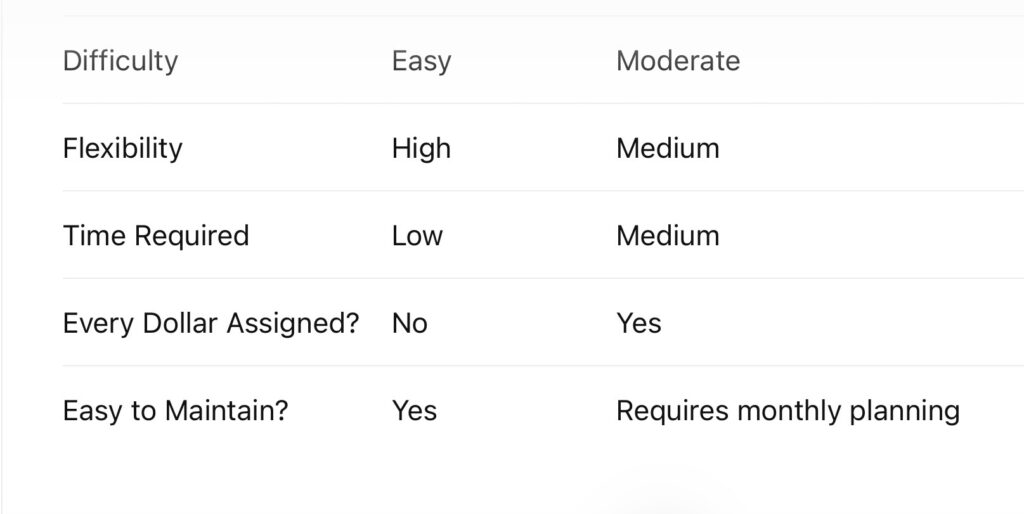

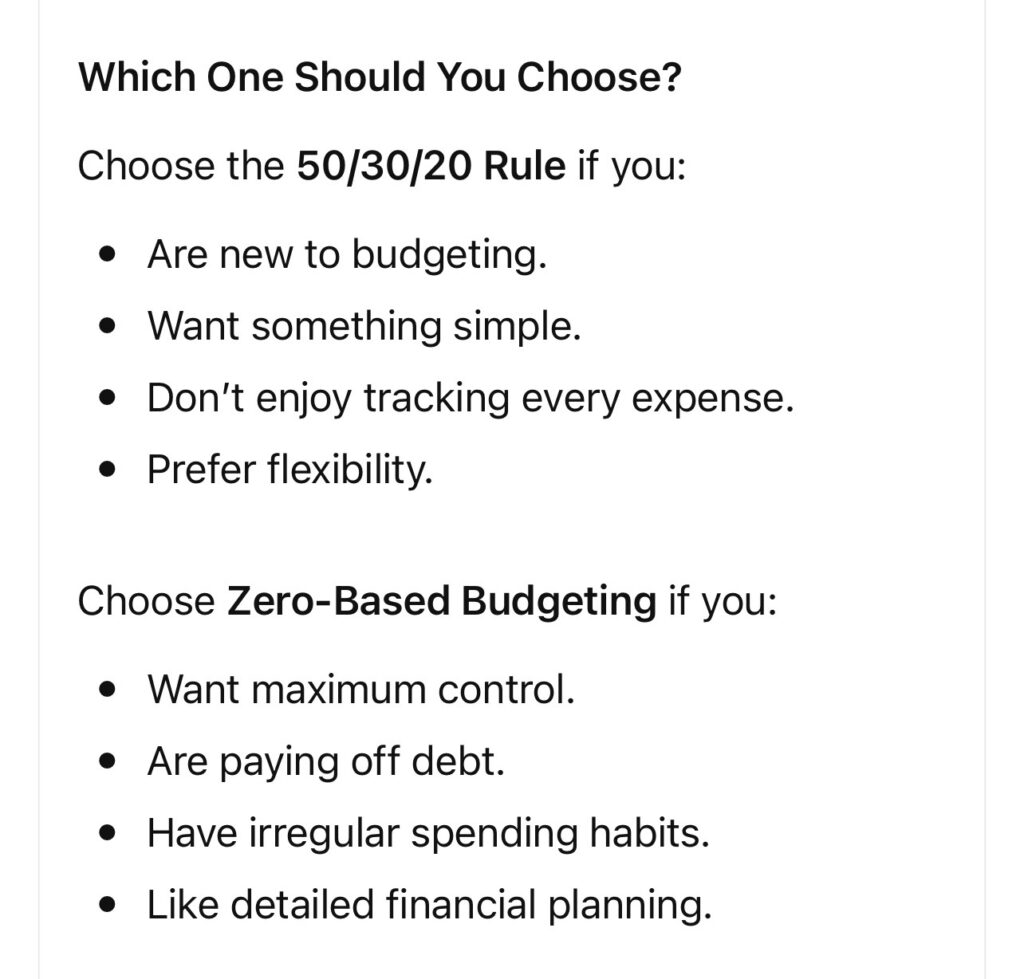

50/30/20 Rule vs. Zero-Based Budgeting

Choosing the right budgeting method depends on your personality and financial goals.

Neither method is better than the other.

The best budget is simply the one you’ll consistently follow.

Best Budgeting Apps in 2026

Technology has made budgeting easier than ever before.

These apps can automatically categorize expenses, track your spending, and help you stay within your budget.

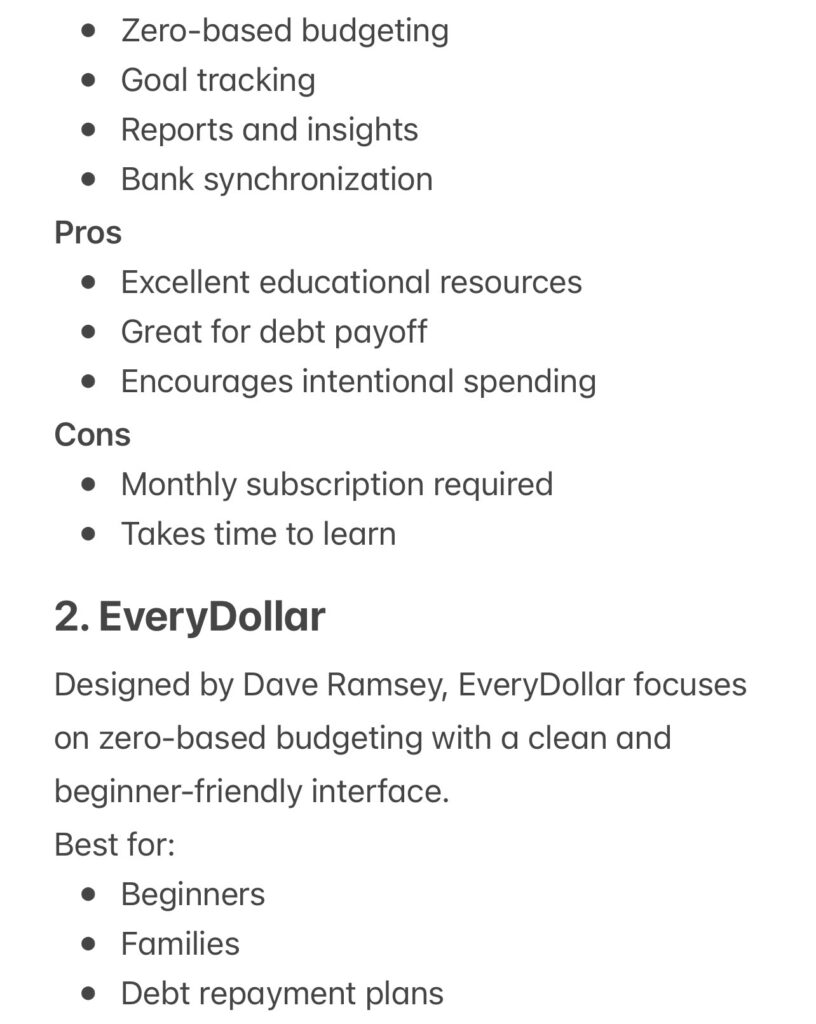

1. YNAB (You Need A Budget)

Best for people who want complete control over their finances.

Features:

3. Goodbudget

Goodbudget uses the traditional envelope budgeting system.

Instead of carrying cash, you divide your money into digital envelopes for different spending categories.

Perfect for:

4. PocketGuard

PocketGuard automatically calculates how much money you have available after paying your bills.

It answers one simple question:

“How much can I safely spend today?”

Ideal for people who often overspend.

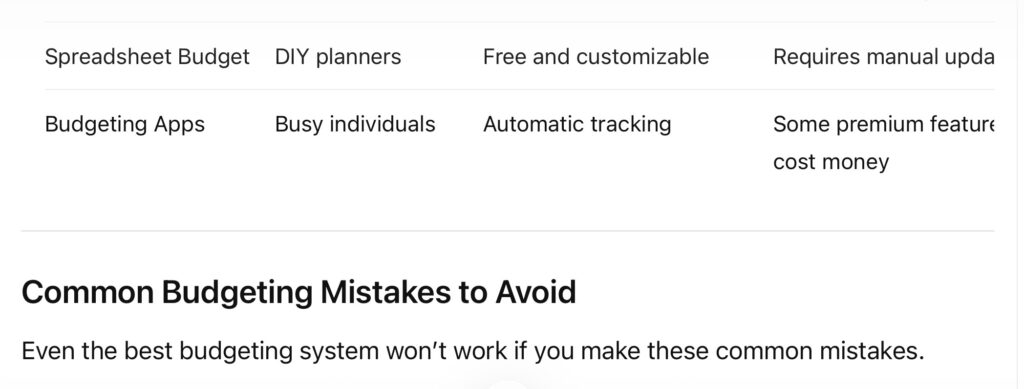

5. Google Sheets or Microsoft Excel

You don’t necessarily need a paid app.

Many people successfully manage their finances using spreadsheets.

Advantages include:

Common Budgeting Mistakes to Avoid

Even the best budgeting system won’t work if you make these common mistakes.

1. Forgetting Small Purchases

Daily coffee.

Snacks.

Food delivery.

Online subscriptions.

These small expenses may seem harmless individually, but together they can quietly consume hundreds of dollars each month.

Track every purchase.

2. Not Having an Emergency Fund

Unexpected expenses are guaranteed.

Without savings, you’ll likely rely on credit cards or loans.

Aim to build an emergency fund covering at least three to six months of essential living expenses.

Start small if necessary.

Even saving a little each month makes a difference.

3. Making Your Budget Too Strict

Completely eliminating entertainment often backfires.

Instead, create a realistic “fun money” category.

Enjoying life while staying within your budget is much more sustainable.

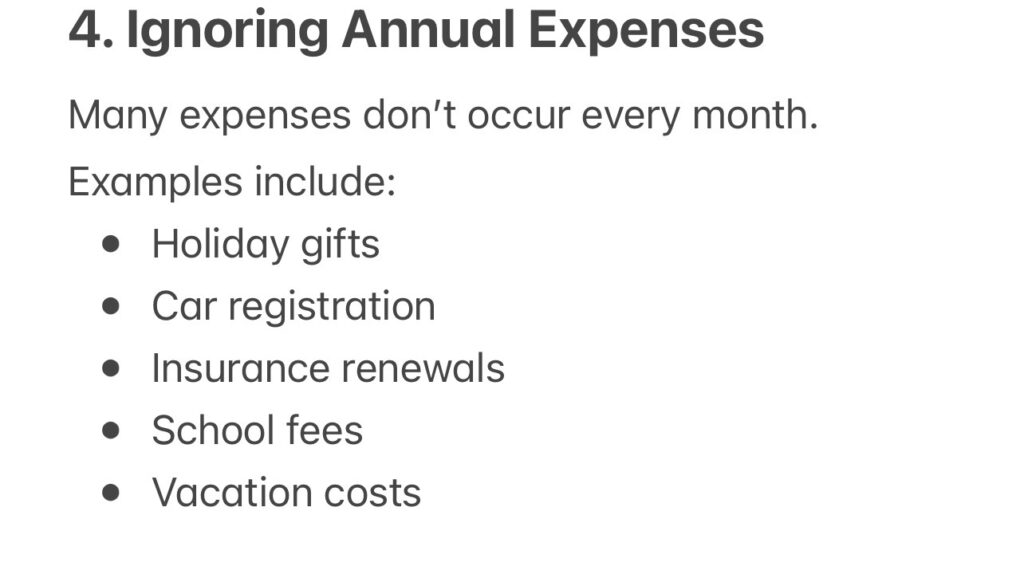

4. Ignoring Annual Expenses

Many expenses don’t occur every month.

Examples include:

Instead of treating these as surprises, divide the total annual cost by 12 and save a portion each month.

5. Never Reviewing Your Budget

Life changes.

Your budget should too.

Review it every month and adjust as needed.

A flexible budget is far more effective than a rigid one.

Actionable Tips to Make Your Budget Stick

Building a successful budget isn’t just about numbers—it’s about creating habits you can maintain.

Here are practical tips to help you stay on track.

Pay Yourself First

Transfer money into your savings account as soon as you receive your paycheck.

Save before you spend.

Automate Your Bills

Automatic payments reduce the risk of missed due dates and late fees.

Review Your Budget Weekly

Spend just 10 to 15 minutes each week checking your spending.

Small corrections are easier than major fixes.

Set Clear Financial Goals

People are far more motivated when they know what they’re working toward.

Examples include:

Positive reinforcement makes budgeting much easier to maintain.

Real-World Examples

Example 1: Sarah’s First Successful Budget

Sarah had tried budgeting several times but always gave up after a month.

Instead of tracking every purchase, she adopted the 50/30/20 rule.

By automating her savings and allowing herself a reasonable entertainment budget, she stayed consistent for an entire year.

By the end of that year, she had saved over $6,000 without feeling deprived.

Lesson

Simple budgets are often easier to maintain than complicated ones.

Example 2: David Eliminates Credit Card Debt

David constantly wondered where his salary disappeared.

After switching to zero-based budgeting, he assigned every dollar a specific purpose.

Within eight months, he paid off his high-interest credit card while also building an emergency fund.

Lesson

Giving every dollar a job helps eliminate wasteful spending and accelerates financial progress.

Example 3: Planning Ahead for Holiday Spending

A family of four used to rely on credit cards every December.

Instead, they created a holiday savings category and set aside a small amount each month.

When the holidays arrived, they paid cash for gifts and celebrations, avoiding debt entirely.

Lesson

Preparing for predictable annual expenses prevents financial stress and helps you stay on budget.

Frequently Asked Questions (FAQs)

1. What is the best budgeting method for beginners?

The 50/30/20 budgeting rule is one of the easiest methods for beginners because it’s simple, flexible, and doesn’t require tracking every single expense. It divides your after-tax income into three categories:

If you prefer more detailed control over your finances, zero-based budgeting may be a better choice.

2. How much money should I save each month?

A common recommendation is to save at least 20% of your income whenever possible. However, if that isn’t realistic, start with whatever amount you can consistently afford—even if it’s just 5% or 10%.

The most important thing is to build the habit of saving regularly.

3. Is budgeting worth it if I have a low income?

Absolutely.

Budgeting isn’t only for people with high incomes. In fact, it can be even more important if your income is limited. A budget helps you prioritize essential expenses, reduce unnecessary spending, and make every dollar work harder.

Even small improvements in your spending habits can make a significant difference over time.

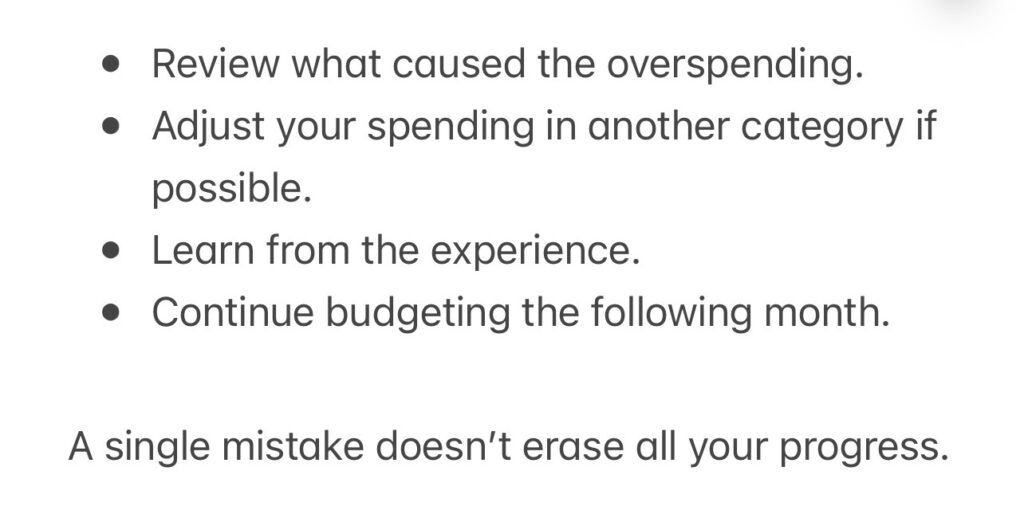

4. What should I do if I overspend?

Don’t panic.

Overspending happens to everyone occasionally.

Instead of giving up on your budget:

A single mistake doesn’t erase all your progress.

5. Should I use cash or a budgeting app?

Both options can work well.

If you’re prone to overspending, using cash with the envelope budgeting method can help you stay disciplined.

If you prefer convenience and automation, budgeting apps can track your expenses, categorize transactions, and provide helpful reports.

Choose the method you’ll actually use consistently.

6. How often should I review my budget?

Review your budget at least once a month.

It’s also a good idea to spend 10–15 minutes each week checking your spending to make small adjustments before they become bigger problems.

7. Can I still enjoy life while following a budget?

Yes.

One of the biggest misconceptions about budgeting is that it eliminates fun.

A realistic budget should include money for entertainment, hobbies, dining out, and other activities you enjoy. Budgeting is about spending intentionally—not eliminating happiness.

8. How long does it take for budgeting to become a habit?

For most people, budgeting becomes much easier after a few months of consistent practice.

The first month is usually the hardest because you’re learning your spending habits. Over time, budgeting becomes a normal part of your financial routine.

Final Thoughts

Creating a budget that actually works isn’t about being perfect—it’s about being intentional.

If you’ve failed at budgeting before, remember that failure doesn’t mean you’re bad with money. More often than not, it means the budgeting system wasn’t realistic or flexible enough for your lifestyle.

The key is to choose a method that matches your personality and financial goals.

If you prefer simplicity, the 50/30/20 rule provides an excellent starting point.

If you enjoy detailed planning and want every dollar to have a purpose, zero-based budgeting may be the better choice.

Whichever method you choose, consistency matters far more than perfection.

Start by understanding your income, tracking your expenses, and setting achievable financial goals. Review your budget regularly, make adjustments when needed, and don’t be discouraged by occasional setbacks. Every month is a new opportunity to improve your financial habits.

Remember that budgeting isn’t about restricting your life—it’s about giving yourself the freedom to spend with confidence, save for the future, and reduce financial stress.

Every dollar you manage wisely today brings you one step closer to financial security, greater peace of mind, and the life you want to build.

The best budget isn’t the most complicated one.

It’s the one you can stick to consistently.

Start today, stay patient, and let your budget become one of the most powerful tools for achieving your financial goals.

Key Takeaways

- A budget is a plan that gives every dollar a purpose.

- Most budgets fail because they are unrealistic, too restrictive, or not reviewed regularly.

- The 50/30/20 rule is ideal for beginners who want a simple budgeting system.

- Zero-based budgeting offers greater control by assigning every dollar a specific job.

- Budgeting apps can simplify expense tracking and help you stay accountable.

- Planning for irregular expenses prevents financial surprises.

- Building an emergency fund should be one of your top financial priorities.

- Reviewing your budget every month helps you stay on track.

- Budgeting is about progress, not perfection.

- Consistent financial habits lead to long-term financial freedom.

How to Build Your First Emergency Fund: A Beginner’s Step-by-Step Plan

- How to Create a Budget That Actually Works (Even If You’ve Failed Before): A Complete Beginner’s Guide for 2026 - July 18, 2026

- Personal Finance for Beginners: A Step-by-Step Guide to Managing Your Money in 2026 - July 17, 2026

- How Long Does It Take to Make Money Blogging? A Realistic Timeline for Beginners (2026 Guide) - July 16, 2026